Greetings!

Today’s edition of Advice for the Good Life touches on something quietly reshaping nearly every corner of modern life: artificial intelligence, health, decision-making, and the growing importance of discernment in an age overflowing with information.

In this week’s Wealth Advisory, we unpack the confirmation of new Fed Chair Kevin Warsh, what his leadership could mean for markets, inflation, interest rates, and investor portfolios, and why maintaining long-term perspective matters far more than reacting emotionally to every Fed headline.

Next, our Wellness Navigator, Christine Despres, delivers an important reminder that your bones are talking long before they break. She shares why women should rethink waiting until 65 for baseline bone density testing, along with practical guidance for building strength, resilience, and long-term healthspan beginning today.

And in Etcetera, we explore the explosive rise of AI-generated financial advice, the opportunities and dangers that come with it, and why financial literacy—and collaboration with a trusted advisor who understands both markets and modern technology—may matter more than ever.

As always, I hope you enjoy today’s edition. If something resonates, please share it with a friend, colleague, spouse, or family member and encourage them to subscribe. This community continues to grow the old-fashioned way: one thoughtful recommendation at a time.

Wealth Advisory: What Kevin Warsh’s Leadership of the Fed Could Mean for the Markets

The Federal Reserve occupies a central position in financial markets and the broader economy, and its influence has expanded considerably over recent decades. From the 2008 global financial crisis to the inflationary pressures of recent years, investors have paid close attention to every Fed decision. It is no surprise, then, that leadership changes at the Fed attract significant attention from investors and the general public alike. At the same time, it is worth understanding what the Fed can and cannot control when it comes to long-term investing.

The Senate has confirmed Kevin Warsh as the new Fed Chair. Warsh is an experienced policymaker who served on the Fed’s Board of Governors during the global financial crisis.1 Markets have largely responded positively to his nomination, as he is regarded as a familiar figure with deep knowledge of the Fed and monetary policy. What could this mean for Fed policy and investor portfolios in the years ahead?

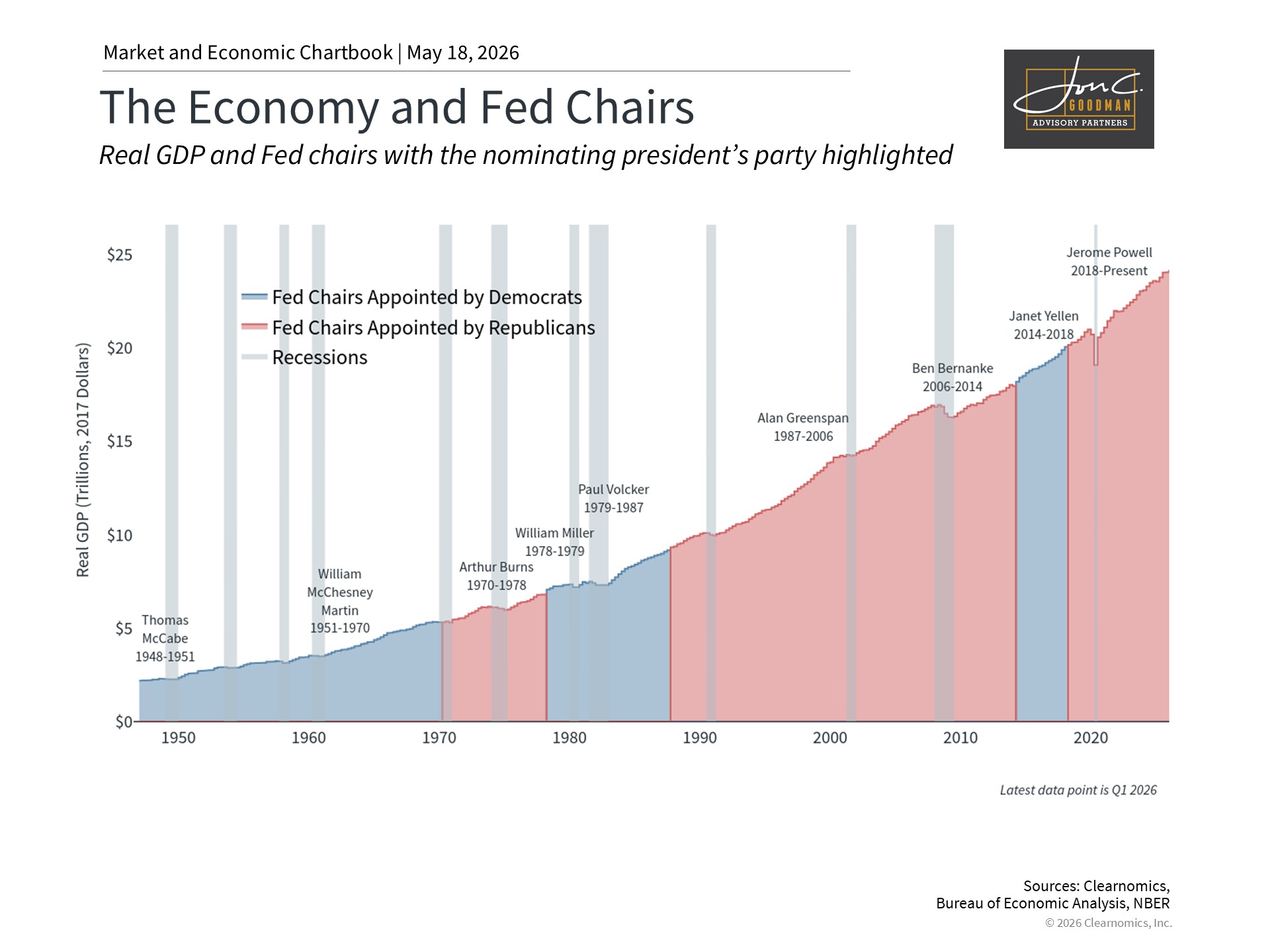

The economy has grown under many Fed leaders

Because Fed leadership transitions are relatively rare, it is helpful to step back and gain some broader perspective. The Chair of the Federal Reserve is nominated to a four-year term, while members of the Board of Governors serve rotating 14-year terms. This structure is designed primarily to insulate monetary, regulatory, and supervisory decisions from political pressures, a principle commonly referred to as “Fed independence,” which has been both tested and debated throughout history.

The accompanying chart illustrates that the U.S. economy has expanded across the tenures of various Fed chairs, regardless of which president nominated them. Paul Volcker, Alan Greenspan, Ben Bernanke, Janet Yellen, and Jerome Powell each confronted distinct economic challenges, ranging from stagflation in the 1970s and early 1980s to the global financial crisis, the pandemic, and the most recent surge in inflation. Throughout these periods, numerous market and economic cycles required the Fed to adapt to new circumstances, sometimes deploying their policy tools in novel ways.

The Fed and interest rates represent only one piece of the puzzle when it comes to economic health. The Federal Reserve Reform Act of 1977 established a “dual mandate” to promote maximum employment and stable inflation, which should ideally produce predictable long-term borrowing costs for consumers, businesses, and the government.

Despite how markets often perceive the Fed, however, the central bank does not control all aspects of the economy. Many of its tools, such as the federal funds rate, are widely regarded as blunt instruments that operate with what economists describe as “long and variable lags.” Economic shocks, technological change, demographic shifts, and global events all play significant roles. For example, the Fed can respond to rising gasoline prices or the impact of AI on the job market, but it cannot directly control either of these forces.

For investors, this means that while the Fed plays an important role and interest rates do influence many parts of the economy and financial markets, placing too much emphasis on each individual Fed decision can result in missing the bigger picture. Focusing instead on the underlying market and economic drivers that the Fed is navigating can help investors maintain a long-term perspective.

Kevin Warsh favors a more narrowly focused Fed

Like all government institutions, the Fed is imperfect and does not have a crystal ball when it comes to forecasting where the economy is headed. In making decisions, policymakers rely on the same public and private economic data available to all economists. It is natural, therefore, that the Fed faces criticism regarding specific policy decisions as well as its broader role as an institution. As with all aspects of investing, it is often important to set politics aside in order to better distinguish what the Fed might do from what observers believe it ought to do.

In his recent Senate testimony, Warsh stated that he favors “a clearer, cleaner match between the Fed’s powers and responsibilities,” signaling a preference for a more focused central bank.2 He also emphasized that “monetary policy independence is essential” and that policymakers must act in the nation’s interest. Historically, Warsh has been characterized as an “inflation hawk,” meaning his policy preference would lean toward higher interest rates to keep inflation in check, as well as promoting reform at the Fed.

From an investment standpoint, there are at least three implications based on his views. First, it will take time to fully understand how Warsh’s current views will shape policy in this inflationary environment, particularly if they come into tension with the White House’s preference for lower rates. He may need to address this as early as his first press conference, given that high oil prices will weigh on upcoming Fed decisions.

That said, this would not be the first time tension has emerged between the executive branch and the Fed. Elected officials naturally prefer lower interest rates to stimulate economic activity. Notable historical examples include conflicts between President Lyndon B. Johnson and Fed Chair William McChesney Martin Jr., Ronald Reagan and Paul Volcker, and most recently Donald Trump and Jerome Powell, among others. Such friction has arisen even when the Fed Chair was appointed by the sitting president.

Inflation and the money supply add complexity to Fed decision-making

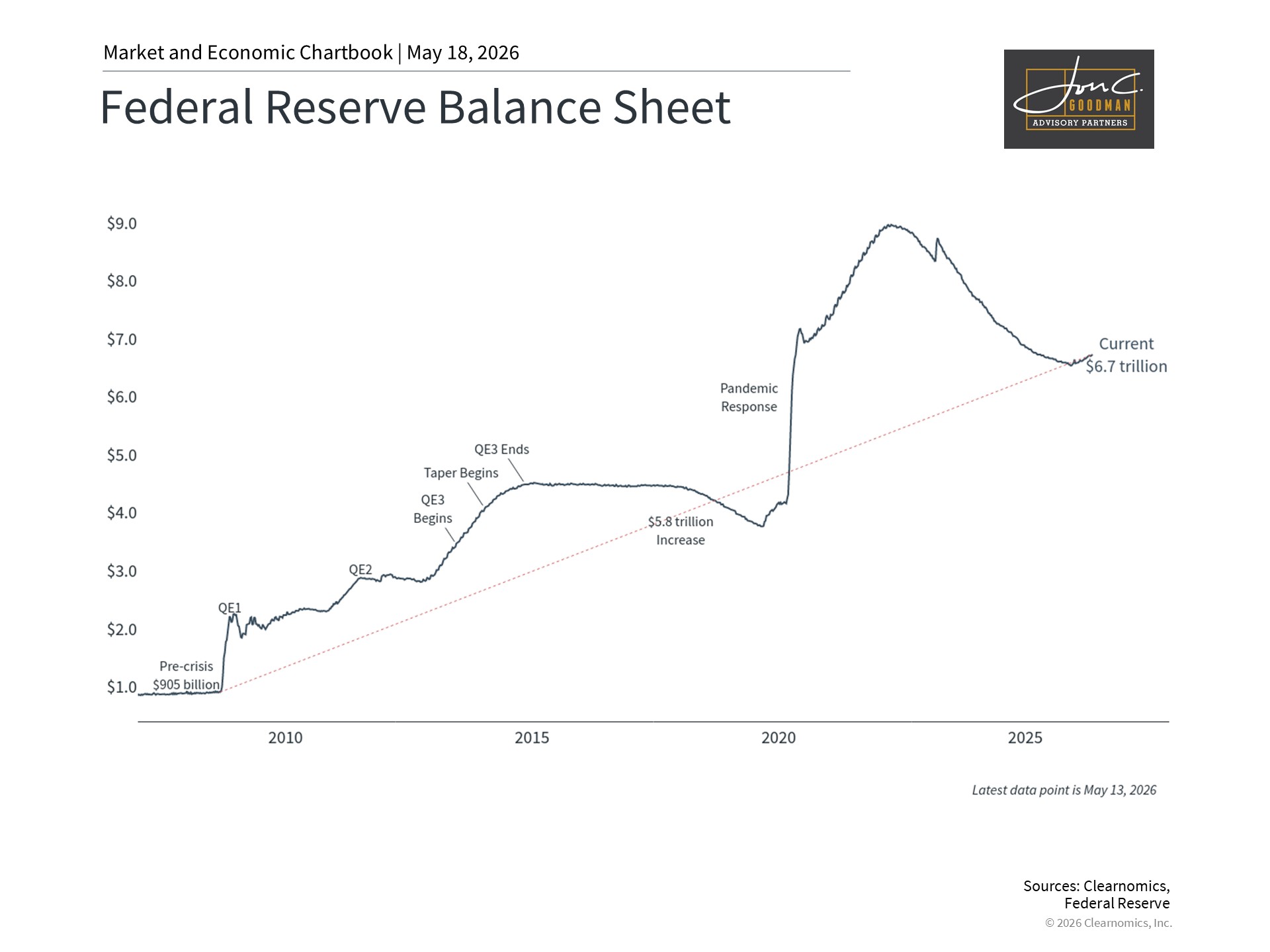

Second, while Warsh has expressed concern that the Fed has overreached with green initiatives and social policies, he has not advocated for sweeping changes to the institution’s core functions. Notably, Warsh believes that crisis-era measures such as the expansion of the Fed’s balance sheet were appropriate, given that he was present when many of those decisions were made.3

e does argue, however, that the Fed should “retrace its steps” once conditions normalize and a crisis has passed. In other words, the Fed’s balance sheet, which remains substantial at $6.7 trillion, is not where it should be now that the 2008 financial crisis and the pandemic are long behind us. In theory, reducing the balance sheet would tighten financial conditions, as it involves either selling or reinvesting less each month in Treasury securities and mortgage-backed securities. This process is commonly referred to as “quantitative tightening,” the reverse of the easing undertaken during crisis periods. Shifts in this policy can affect bond prices, mortgage rates, and corporate borrowing costs.

Third, Warsh believes that Fed policy, particularly since the pandemic, has contributed to the growth of the federal deficit and national debt. Much as with the Fed’s balance sheet, he contends that while spending may be warranted during recessions, it should be symmetric, and monetary policymakers should avoid weighing in on fiscal matters.4

Of course, the Fed does not directly control federal spending, and it remains unclear what the new Fed Chair would do differently to influence budgets passed by Congress. To the extent the Fed does comment on the size of the budget deficit, it would likely do so through guidance or by managing interest rates. For investors, this is another reason why policy rates may continue to depend on a wide range of factors in the years ahead.

The new Fed Chair inherits a particularly challenging economic environment. Inflation has picked up in recent months due to higher oil and gasoline prices, driven by the war in Iran. Headline CPI was 3.8% year-over-year as of April 2026, with core CPI at 2.8%, both still above the Fed’s 2% target.

This has created a difficult policy backdrop. While many at the Fed and in markets had previously anticipated further rate cuts, fed funds futures now reflect the possibility that the Fed may need to consider a rate increase by early 2027. These market expectations should be interpreted with caution, as they shift frequently in response to new economic data and global developments. Nevertheless, they underscore the uncertain path ahead for monetary policy.

For investors, the most important takeaway is that markets and the economy have performed well across many different Fed leadership transitions and policy environments. Changes at the top of the Fed naturally generate uncertainty, but they rarely alter the long-term fundamentals that drive financial markets. Earnings growth, productivity, demographics, and innovation remain the most important drivers of long-run returns.

The bottom line? As Kevin Warsh takes over as Fed Chair, it’s important to maintain perspective on the role of the Fed. Ultimately, understanding the longer-term drivers of the market and economy is the best way to achieve financial goals.

References

- https://www.senate.gov/legislative/LIS/roll_call_votes/vote1192/vote_119_2_00120.htm

- https://www.banking.senate.gov/imo/media/doc/warsh_testimony_4-21-26.pdf

- https://www.wsj.com/opinion/the-high-cost-of-the-feds-mission-creep-role-responsibility-monetary-policy-economy-20a352f8

- Ibid.

Wellness Navigator and Holistic Brain Health Coach, Christine Despres, RN,NBC-HWC, CDP

Your Bones Are Whispering. Are You Listening?

May is Women’s Health Month and I’m showing up in your inbox today as your wellness bestie with a few friendly but firm reminders.

When did you last look at your actual health goals for this year? Not the ones you thought about in January, but the real ones. The appointments you’ve been meaning to schedule, the tests you’ve been putting off, the numbers you’ve never actually checked.

This month is a good reason to pull that list back out.

I want to talk today about one specific test that most women aren’t getting until it’s far too late. And if you’ve been waiting for a nudge, consider this.

Waiting Until 65 Is Too Late

By the time you reach 65, you may have already lost a significant amount of bone mass during the years you weren’t paying attention.

Bone loss doesn’t announce itself. There’s no pain, no obvious symptoms, no warning until something breaks. And the window where you have the most power to intervene is not in your mid-sixties. It’s now.

Brain health experts and integrative medicine physicians increasingly recommend that women get a baseline DEXA scan when they enter perimenopause or menopause, typically in their mid-forties to mid-fifties.

That baseline is everything.

It tells you where you’re starting from, it gives you something to measure against and it creates urgency while you still have time to act.

Waiting a decade to get that number is not caution. It’s a missed opportunity.

The same hormonal shift that affects your brain, your metabolism, your sleep and your energy is also quietly affecting your bones.

Estrogen plays a protective role in bone density and as it declines through perimenopause and menopause, bone loss accelerates. This is not a frailty story. This is a biology story.

My Own Numbers

I’ll be transparent with you.

My own recent bone density scan came back showing mild osteopenia.

Here’s the part that stopped me in my tracks: my primary care doctor hadn’t ordered the test. I had to request it myself after consulting with a brain health expert.

Osteopenia affects nearly one in two women over 50.

Osteopenia is the warning. Osteoporosis is what happens when you ignore it.

And osteoporosis is what leads to the fractures, the lost height, the broken hip that changes everything. That is not the woman you are planning to be.

A proactive approach to your healthspan starts now.

Here’s what I’m prioritizing:

- Heavy weight strength training

- Leaning harder into my weighted vest walks

- Hitting my calcium and protein targets daily

- Adequate Vitamin D supplementation and sunlight

Not because I needed another thing on my list. Because it matters.

The Calcium Gap

Women over 50 need 1,200 mg of calcium daily. Most of us are getting closer to 700 to 800 mg, which means there’s a real gap. If you’re supplementing, it’s complicated. Diet is a better source.

Top eight food sources worth building into your week:

- Low-fat plain Greek yogurt, 300 to 400 mg per cup

- Wild salmon, 325 to 350 mg per three ounce serving

- Parmesan cheese, around 330 mg per ounce

- Calcium-set tofu, 200 to 430 mg per half cup. Check the label as calcium content varies significantly by brand.

- Cooked collard greens, around 270 mg per cup

- Cooked kale, around 180 mg per cup

- White beans, 130 mg per half cup

- Cooked bok choy, around 100 mg per cup

Where Coaching Comes In

What I see most often in my work is that women have the best intentions and then life gets in the way.

That’s not a willpower problem. That’s a support problem.

Having someone in your corner to keep you accountable and on track is what makes the difference. The women aging with the most strength, mobility, and clarity are doing the same things for their bones and their brain.

Moving with intention, eating to nourish, sleeping like it’s their job. If you haven’t had a DEXA scan yet, ask your doctor for one. Know your baseline. Then let’s talk about what to do with it.

And if you’re ready to start investing in your greatest assets, I’d love to be your guide.

👉 Book a free Brain Health Strategy Session here: Click Here to Schedule Your 30 minute Strategy Call

With strength,

Christine

The Wellness Navigator | Holistic Brain Health Coach | RN, NBC-HWC, CDP

https://www.thewellnessnavigator.com/

A recent article in Financial Advisor Magazine reported that nearly half of Americans are now turning to artificial intelligence for financial advice. That number alone says something important: AI is no longer coming. It’s here. And for many people, it has already become the first stop for questions about budgeting, debt, investing, taxes, and retirement planning. (Wikipedia)

There is real upside to this shift.

AI can explain concepts quickly, summarize information, compare strategies, and help people engage with subjects that once felt intimidating or inaccessible. Used properly, it can improve efficiency, organization, and even financial literacy itself. Many advisory firms are now using AI behind the scenes to improve client service, meeting preparation, planning workflows, and communication. (Financial Planning)

But there is also growing concern about overreliance.

AI’s responses are only as good as the questions being asked, the assumptions built into the prompts, and the data available to the model. Even then, users often have no idea what may be outdated, oversimplified, missing, or simply wrong. One recent survey found that 62% of Americans still do not fully trust AI-generated financial information. (Yahoo Finance)

Behaviorally, there are risks too.

AI systems tend to affirm people rather than challenge them. That may feel good emotionally, but it can be dangerous financially. MarketWatch recently highlighted research showing AI-generated investment advice is significantly more likely to reinforce “action bias,” encouraging investors to trade, react, or “do something” when patience and discipline may actually be the wiser course. (MarketWatch)

This is precisely why financial literacy matters more than ever.

The better your understanding of risk, diversification, taxes, debt, cash flow, and long-term compounding, the better your questions become. And the better your questions become, the more useful AI can become as a tool rather than a trap.

Which is also why collaborating with a trusted advisor matters more than ever.

The future likely isn’t human advice versus artificial intelligence. It’s human wisdom enhanced by technology. Advisors who understand both financial planning and how to intelligently use AI tools may ultimately offer the best of both worlds: efficiency plus judgment, data plus discernment, speed plus context.

AI can process information. But experienced advisors help families think clearly, pressure-test assumptions, avoid emotional mistakes, recognize blind spots, navigate complexity, and align financial decisions with real human goals and values.

And in a world increasingly flooded with information, discernment may become the most valuable asset of all.

That’s all for today.

Thank you for your time, trust, and readership.

Warmly,