Greetings!

Welcome to this week’s edition of Advice for the Good Life—your weekly guide to wealth, wellness, and wisdom. We’ve set the table with a full plate of insights to nourish your finances, health, and mind.

In Wealth Advisory, we break down how surging gasoline prices are squeezing household budgets (due to the conflict in Iran) and what that means for your investments and the inflation outlook.

Next, in Wellness Navigator, Christine Despres shares this year’s “Dirty Dozen” list so you’ll know which foods to buy organic and which are safe to buy conventional. She also invites you to a free Brain Boost session on April 1 to tackle stress—an essential step for better health and a sharper mind.

And finally, in Etcetera, our special guest contributors—economists Brian Wesbury and Robert Stein—offer a candid economic outlook. They discuss why a one-two punch of slowing consumer spending and global oil turmoil could spell trouble ahead, and what might help keep growth on track.

Enjoy this week’s edition, and if you find value in these insights, please share it with friends and encourage them to subscribe. Thank you for joining us on the journey to a wealthier, healthier, and wiser life!

Wealth Advisory: How Rising Gasoline Prices Affect Consumers and Investors

For most Americans, the price of gasoline at the pump is one of the most direct ways the conflict in Iran touches their daily lives. Fuel prices are prominently displayed and updated frequently, and filling up at least once a week is a basic necessity for commuting to work, school, and running everyday errands. Diesel prices are equally significant, as they influence the transportation and manufacturing costs of goods throughout the broader economy. This is precisely why fuel prices serve as critical economic indicators, and why the evolving situation in the Middle East has become an increasing concern for consumers and investors alike.

As the conflict enters its second month, with new headlines ranging from proposed peace agreements to potential escalation on a daily basis, oil prices remain elevated with substantial intraday swings. Brent crude is now trading above $110 per barrel and WTI above $100, signaling that higher energy prices will weigh on household budgets, inflation metrics, and Federal Reserve policy decisions.

The energy crisis of the 1970s is perhaps the most frequently cited historical example of how elevated oil prices can reshape consumer behavior and the broader economy for years. During that decade, two separate oil embargoes resulted in long lines at gas stations, fuel rationing, and a fundamental shift in how Americans approached energy consumption and national energy security.

Fortunately, the current environment differs in several meaningful ways. The lasting legacy of the 1970s and early 1980s included a wave of investment in domestic energy production and fuel efficiency measures that have meaningfully reduced the U.S. economy’s sensitivity to oil price spikes. The U.S. is now the world’s largest oil producer, inflation had been on a downward trajectory before this shock, and markets have historically adapted and moved forward once the initial disruptions have subsided. While consumers may continue to face headwinds, perspective and patience remain essential for long-term investors.

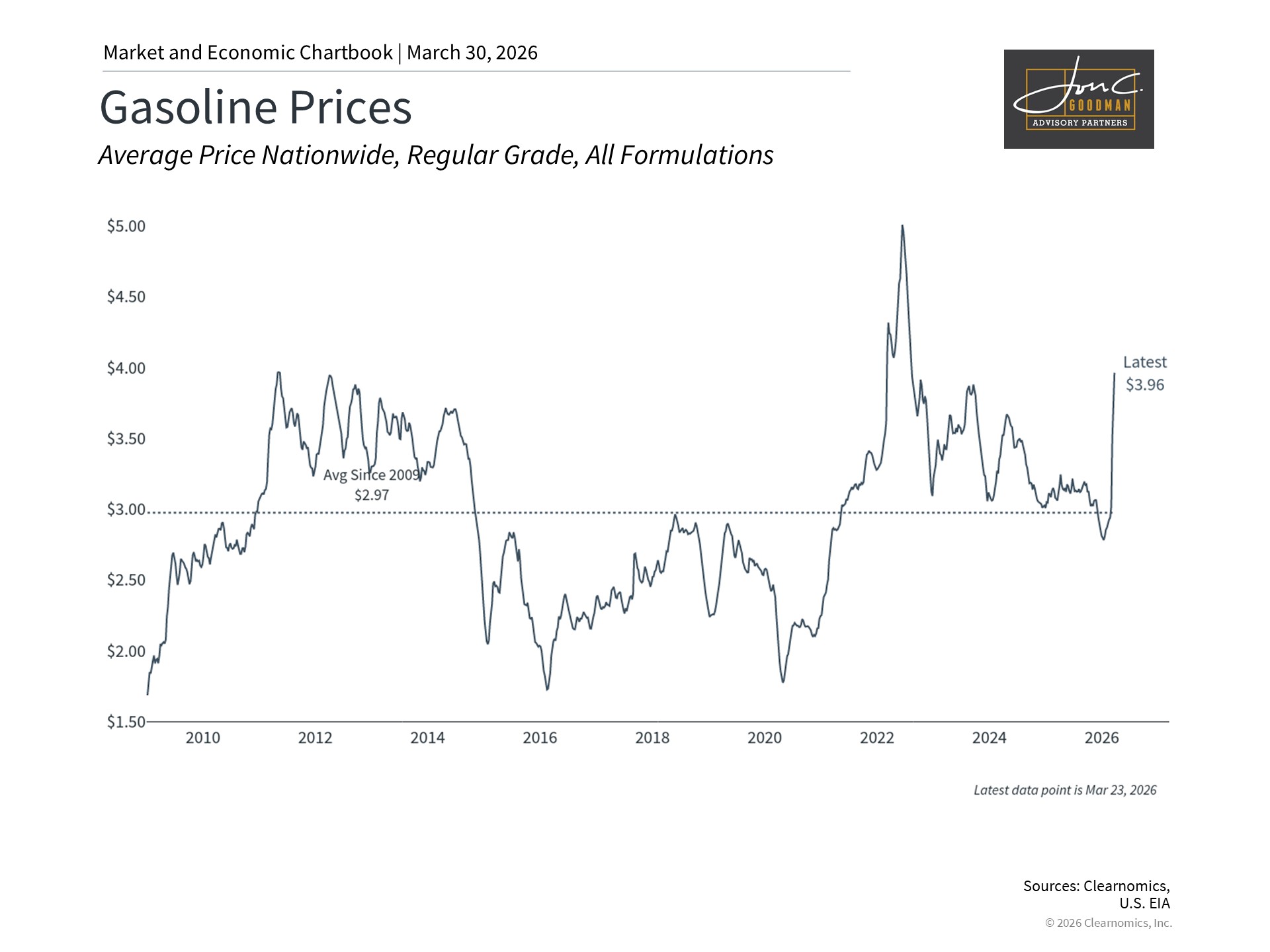

Gasoline prices at the pump have climbed sharply in recent weeks

The national average for regular unleaded gasoline has risen to approximately $4.00 per gallon, an increase of more than a dollar per gallon in just one month. While this remains below the record high of $5.00 per gallon reached in 2022, the situation could deteriorate further if oil prices stay elevated. For most households, filling up the car is a non-negotiable expense. Although drivers may reduce their mileage somewhat, higher gasoline prices will have a direct impact on discretionary spending and savings. Even with the growing adoption of electric vehicles, the majority of cars on the road today still run on gasoline, meaning that higher prices at the pump affect nearly every household budget across the country.

The impact of higher gasoline prices on consumers is both direct and indirect. A straightforward back-of-the-envelope calculation illustrates how rising prices affect everyday consumer spending across different income levels. Assuming the average fill-up is 15 gallons, the current price increase adds $15 to each visit to the gas station. For drivers who fill up once a week, this translates to roughly $780 less in their pockets per year.

At the federal minimum wage of $7.25 per hour, this would represent more than two additional hours of work just to maintain the same financial footing. The picture looks somewhat different for those at higher income levels. The median American household earns just over $70,000 per year after taxes, according to the latest Census Bureau statistics, meaning the added fuel cost represents above 1% of after-tax income. While this leaves less room for discretionary spending or savings, most households at this income level can likely absorb the added cost without severe financial difficulty.

In this sense, higher gasoline prices effectively act as a direct burden on consumers. Without minimizing the challenges that some households may face, it is also evident that most will be able to manage through this period.

From an investment standpoint, the drag on the broader economy can be meaningful. When multiplied across millions of households filling up week after week, the cumulative impact on consumer spending and savings rates can be significant if oil prices remain elevated for an extended period. Beyond the direct consumer impact, the indirect effects may ultimately be even more consequential. Gasoline and diesel fuel are foundational inputs into nearly everything the economy produces. Transportation, manufacturing, agriculture, and distribution all rely on energy, which means that higher fuel costs raise the price of goods and services across the board. This is why oil price spikes do not simply affect energy bills but can ripple throughout the economy over time.

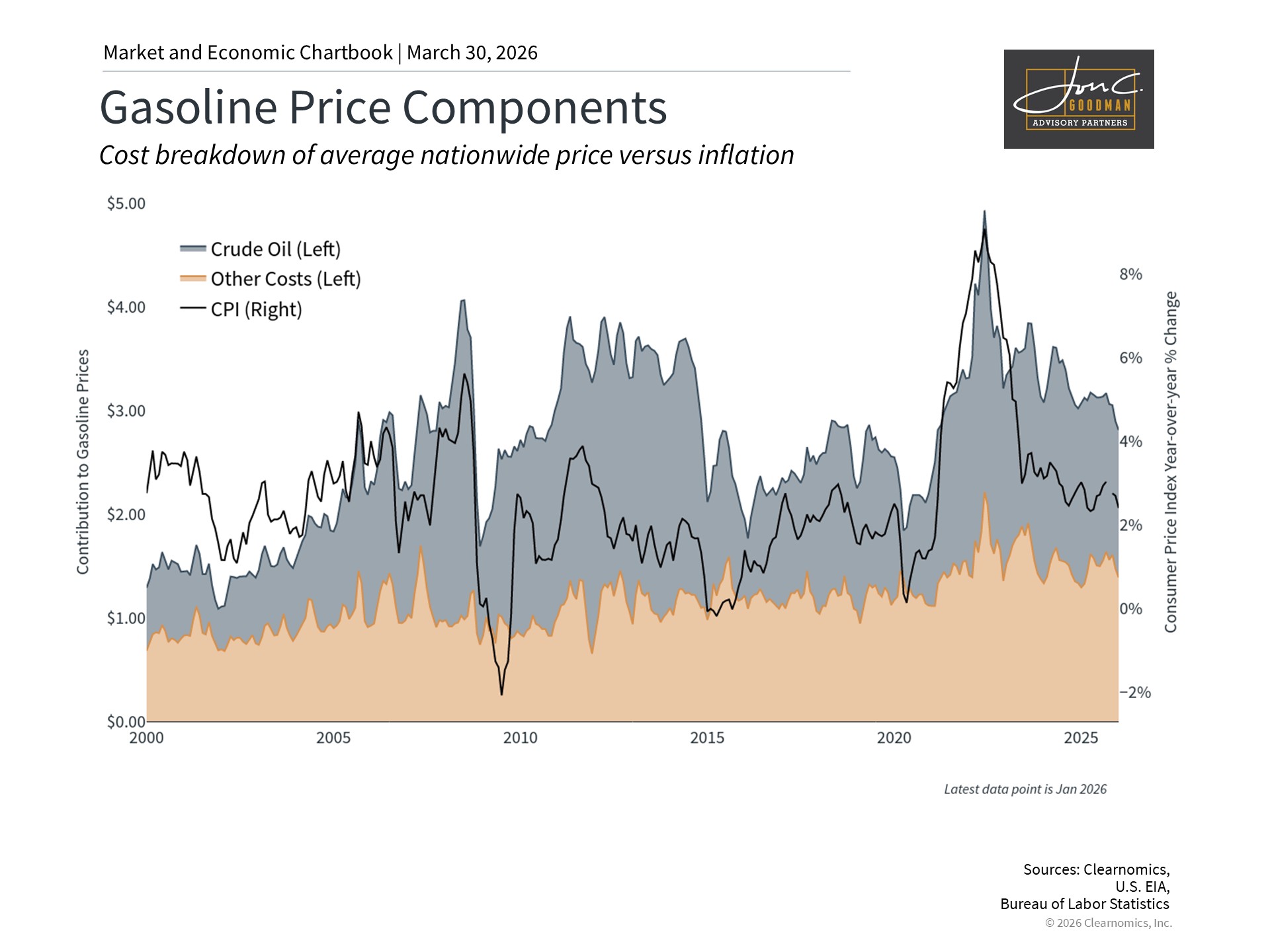

Gasoline prices are shaped by more than just the cost of crude oil

Understanding the factors that drive gasoline prices can help put the current environment in perspective. According to the U.S. Energy Information Agency, approximately half of the price at the pump reflects the cost of crude oil itself. The remaining half consists of refining costs, transportation and distribution to gas stations, sales and marketing expenses, and federal and state taxes.

These additional costs also explain why consumers in certain states pay considerably more than the national average. The accompanying chart, based on the latest available data which does not yet capture the most recent price jump, illustrates how these components have evolved over time.

This breakdown is partly why there is not a one-to-one relationship between crude oil prices and what consumers pay at the pump. It also takes time for higher market prices, which adjust rapidly in the futures market, to be reflected in what consumers actually experience. The chart further highlights the annual change in the overall Consumer Price Index and its clear connection to oil price movements over time.

For investors, it is also worth noting that the oil futures curve is currently deeply “backwardated.” This technical term indicates that oil prices are significantly higher today than they are expected to be in the future, a notable shift from just a month ago when the curve was relatively flat. In other words, while current spot prices reflect the supply disruption stemming from the Middle East conflict, traders are also signaling that they expect oil prices to eventually fall once conditions stabilize. This does not guarantee a swift resolution and can change as new information emerges, but it does suggest that markets view the current spike as a temporary shock rather than a permanent structural shift toward higher prices.

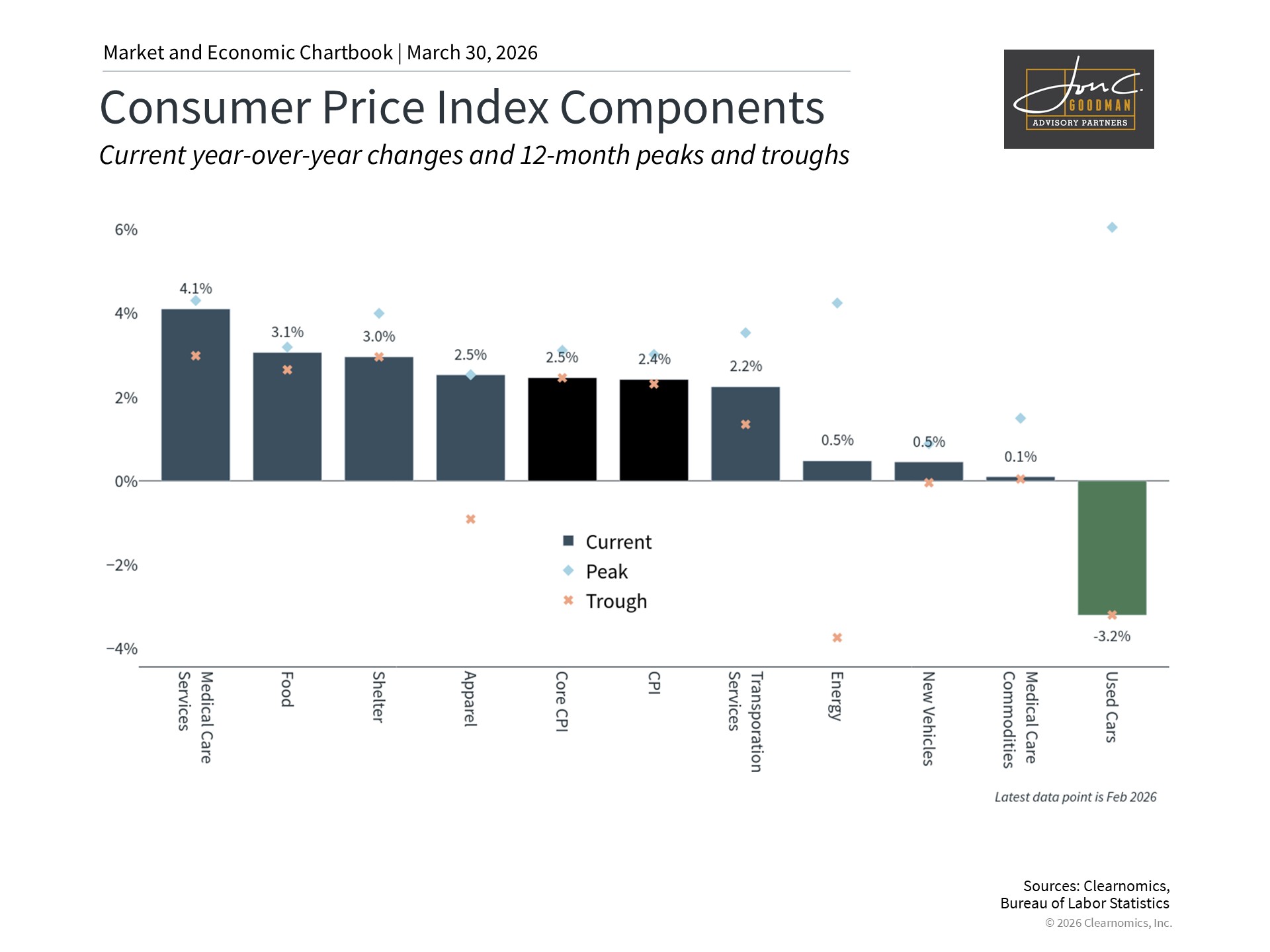

Elevated energy prices add complexity to an already challenging inflation outlook

For investors, energy prices will have a direct impact on headline inflation, as these costs represent important components of the headline Consumer Price Index. After several years of improving energy CPI readings, the recent surge in oil and gasoline prices will almost certainly push headline inflation higher in the months ahead. Organizations such as the OECD now estimate that U.S. inflation could rise faster than previously expected this year.

This development matters for several reasons. First, consumers are still recovering from the inflation surge that followed the pandemic. Second, both stocks and bonds have historically faced headwinds when inflation rises unexpectedly, as higher costs weigh on corporate earnings and erode the real value of fixed income payments. That said, markets have demonstrated considerable resilience over recent years even in challenging inflationary environments.

Third, and perhaps most immediately relevant for financial markets, rising inflation complicates the Federal Reserve’s decision-making process. Markets have already adjusted their expectations, with traders now assigning a higher probability to the Fed holding rates steady or even raising them rather than cutting. This shift in expectations has introduced additional uncertainty for both equity and bond markets, particularly as the Fed undergoes a leadership transition in mid-May.

Economists generally regard these types of “supply-side” shocks as temporary in nature. This is not a prediction that elevated oil prices will be short-lived, per se, but rather reflects the view that high oil prices should moderate once supply comes back online.

While the current environment remains challenging for consumers, it is meaningfully different from the 1970s. Notably, the U.S. is the world’s largest oil and natural gas producer, and the Federal Reserve has considerably more credibility in anchoring inflation expectations today, making the current economic and financial market environment more stable than in prior decades. For investors, this reinforces the importance of remaining invested with a well-constructed portfolio and financial plan. This approach served investors well during the last inflation spike in 2022, and remains the most reliable path toward achieving long-term financial goals.

The bottom line? Rising gasoline prices are a burden for consumers and will likely drive headline inflation higher. However, history shows that markets and the economy have navigated past energy shocks. Investors should maintain a long-term perspective, avoid overreacting to daily headlines, and stay focused on their financial plans.

Wellness Navigator and Holistic Brain Health Coach, Christine Despres, RN, NBC-HWC, CDP

What to Buy Organic (And What’s a Waste of Money)

The Environmental Working Group just released its annual Shopper’s Guide to Pesticides in Produce and this year’s findings are worth noting. Nearly 75% of non-organic fresh produce sold in the U.S. contains residues of potentially harmful pesticides, including PFAS “forever chemicals.” These aren’t pesticides that wash off. They’re called forever chemicals because they accumulate in your body over time and they’ve been linked to hormone disruption, thyroid dysfunction and nervous system damage. Your brain and your body suffer from these chemicals.

Good news though: this is about getting the most bang for your buck. You don’t have to buy everything organic to make a real difference.

The skin rule is your best friend. If you’re eating the skin or outer leaves, that’s where pesticide residue concentrates most. That’s where you want to prioritize organic. If you’re peeling it before you eat it, conventional is usually fine.

The 2026 Dirty Dozen: Buy Organic When You Can

These had the highest pesticide residues, many averaging four or more different pesticides per sample. If you eat these regularly, organic matters most here.

Strawberries · Spinach · Kale, collard and mustard greens · Peaches · Nectarines · Apples · Bell and hot peppers · Cherries · Blueberries · Green beans · Blackberries · Potatoes

Two newcomers this year: blackberries and potatoes. Blackberries tested positive for cypermethrin, a possible human carcinogen. Ninety percent of potato samples contained chlorpropham, a sprout inhibitor banned in the European Union since 2019.

The 2026 Clean Fifteen: Conventional Is Fine

Nearly 60% of these samples had zero detectable pesticide residues. Shop conventional here without worry.

Pineapple · Sweet corn · Avocados · Papaya · Onions · Frozen sweet peas · Asparagus · Cabbage · Cauliflower · Watermelon · Mangoes · Bananas · Carrots · Mushrooms · Kiwi

Two new faces here too: bananas and cauliflower, both with notably low pesticide toxicity.

A word on frozen: If strawberries, blueberries, peaches, or cherries are out of season and organic isn’t available or affordable, go frozen. Frozen produce is picked and flash-frozen at peak ripeness, so the nutrients are intact and the pesticide load is often lower than fresh conventional. Your brain wins either way.

Bottom line: You don’t have to overhaul your grocery budget. Just use this list, eat the rainbow, and when in doubt, frozen organic is a great option year-round.

Source: EWG Shopper’s Guide to Pesticides in Produce, 2026

Which brings me to April. Our next Brain Boost session is Wednesday, April 1st at 10am ET and we’re talking stress management — because stress is one of the biggest drivers of inflammation, cognitive decline and yes, weight gain. Now we’re going to talk about what to actually do about it. It’s free, it’s virtual, and it’s 30 minutes. Grab your spot at the link below — I’d love to see you there.

You made it through a whole month of nutrition content. I hope something landed. Now go find those fresh, local fruits and veggies!

Happy Spring!

Christine

RN | Board-Certified Health & Wellness Coach | Certified Dementia Practitioner | Holistic Brain Health Coach | Nutrition Coach

- If you’re ready to start investing in your greatest asset, I’d love to be your guide.

👉 Book a free Brain Health Strategy Session here: Click Here to Schedule Your 30 minute Strategy Call

https://www.thewellnessnavigator.com/

Stocks See Troubles Brewing

Brian S. Wesbury, Chief Economist

Robert Stein, Deputy Chief Economist

Date: 3/30/2026

The US economy grew a pedestrian 2.0% last year and the Atlanta Fed’s GDP Now is currently projecting real GDP growth at a 2.0% annual rate in the first quarter. If anything, we think there is more downside risk than up to the first quarter projection.

Yes, we are well aware of the ongoing revolution in AI and the benefits this could have for productivity growth. But the federal government remains substantially larger than it was pre-COVID and even more so than it was prior to the Global Financial Crisis. This remains an albatross around the economy’s neck…holding back investment and reducing potential growth.

Meanwhile, there are numerous reasons to be concerned with the economy. What many call the “K-Shaped Economy,” which is just a cute way of talking about inequality, may no longer be providing support for economic growth. The Federal Reserve’s extremely loose monetary policy of 2020-21 artificially held down interest rates and lifted asset prices, which helped those who owned assets. Meanwhile, those who held few assets had their budgets hit hard by the inflation caused by easy money.

Moody’s Analytics estimates that the top 20% of earners are driving a “luxury economy” and are responsible for 63% of total US spending. Stock and home prices are up sharply in recent years, which has likely driven “wealth effect” spending.

But at the Friday close, the S&P 500 is back to where it was eight months ago. If this continues, it could have a negative impact on the consumer spending growth that’s been happening on the upper end of the income spectrum.

This is worrisome because we already see stress at the lower end. The New York Fed says that 5.21% of auto loan balances are 90+ days delinquent, the second highest level going back to at least 1999, even higher than for most of the so-called Global Financial Crisis in 2008-09. The share of credit card balances that are 90+ days delinquent is 12.70%, the highest since 2011. Meanwhile, student loan delinquencies have soared now that COVID-era repayment amnesties are over. If both limbs of the “K” sag, the economy could be in trouble.

Add to this, the fact that Iran seems unwilling to capitulate. If the Fed isn’t on hold, and cuts rates, this risks inflation. Both are bad for the market. We hope that the war ends soon, but President Trump may now be caught between his natural inclination to avoid a prolonged conflict and a desire to show that fear of the TACO trade (“Trump Always Chickens Out”) can’t bully him. This is especially true if the Trump team thinks Iran is counting on rising oil prices and falling stocks to force the US to back off.

The US is now a net petroleum exporter and gets only a small share of its oil from the Middle East. But there are many other countries, especially western advanced economies, that are highly dependent on Middle East oil and other raw materials. These countries are already under stress with the Strait of Hormuz essentially closed. If war continues, this pain will intensify and growth will slow. If western trading partners suffer, that’s an additional headwind for US growth.

And don’t forget troubles in private credit markets. We don’t see a systemic crisis, but clearly this is a problem, and could further diminish investment flows.

The recent drop in US stocks is nothing like the “Liberation Day” mini-panic in early 2025. This time around, it’s less panic and more of a measured reassessment of the headwinds facing the US economy. The market needs a lot of things to go right to find its footing again. Including a smaller government. The odds of that happening in the near-term seem less than stellar.

That’s all for today.

Have a great week,